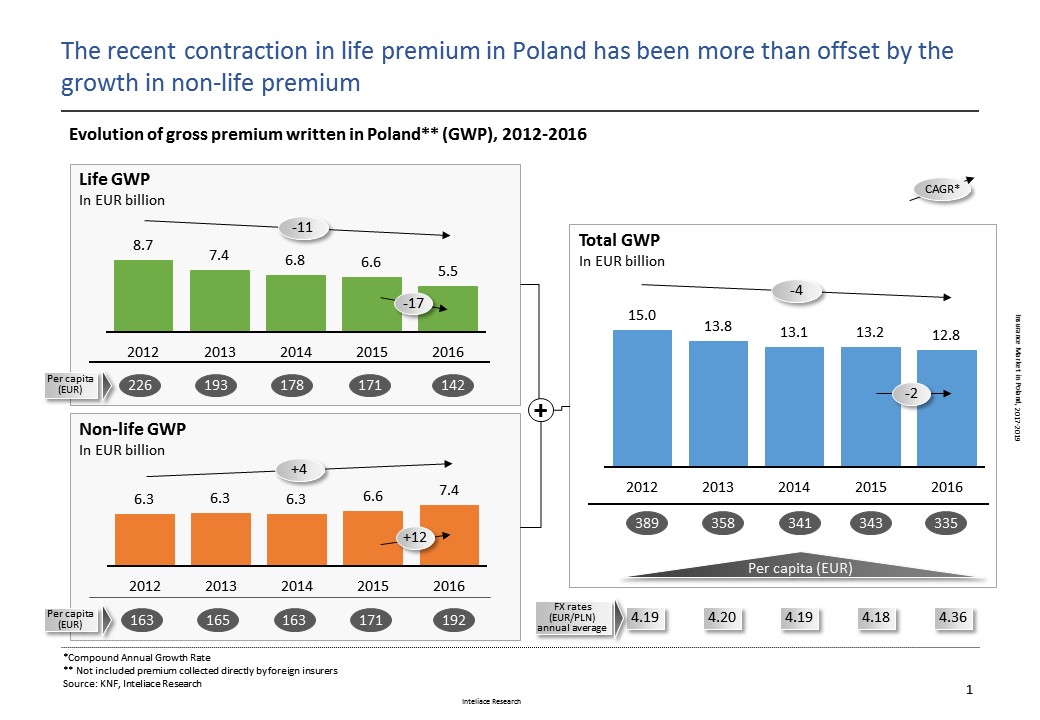

Poland has the largest insurance sector in the CEE with nearly € 13 billion in premium written p.a. and a 40 % regional GWP share.

After overcoming the recent stagnation, total insurance premium in Poland is expected to increase at ~7% p.a. through 2019.

The non-life insurance segment is likely to continue the fast growth driven by increasing tariffs and a higher number of contracts. Also the improving situation of enterprises is expected to fuel more demand for specialized insurance products in the corporate sector including property insurance.

A rebound in new premium is expected to take place in the life business, after a tighter regulatory regime is fully implemented in 2017.

Considering the extremely high competition among insurers and a persisting trend for higher claims, it is expected that profitability of insurers will improve only slightly in 2017-2018.

For more information on recent developments in the Polish insurance sector, please refer to the full publication.

Table of contents

Slide 1: Executive summary

1. Macroeconomic overview Slide 2: Poland - General overview

Slide 3: Poland in Europe: Number of households vs. wealth, 2015/2016

Slide 4: Key macroeconomic indicators, 2011-2016

Slide 5: Foreign trade statistics, C/A, FDI, 2011-2016

Slide 6: Unemployment and salaries/wages, 2011-2016

Slide 7: Disposable income in households and income distribution, 2011-2016; Income distribution 2015

Slide 8: Consumer confidence index evolution, 2011-Feb. 2017

Slide 9: Warsaw Stock Exchange - Turnover, Market cap. and indexes, 2011-2016

Slide 10: Banking assets evolution, 2011-2016

Slide 11: Top 12 foreign investors in banking sector and their subsidiaries, 2016

2. Insurance market Slide 12: Insurance Markets in CEE – Size vs. growth matrix, 2014-2016

Slide 13: Insurance premiums per capita & premiums/GDP penetration – CEE comparison, 2016

Slide 14: Insurance gross premiums - Local insurers (life/non-life, in EUR), 2012-2016

Slide 15: Insurance gross premiums - Local insurers (life/non-life, in PLN), 2012-2016

Slide 16: Top 12 insurance groups in Poland by total premium written, 2016

Slide 17: Insurance market concentration and Herfindahl-Hirschman Index (life/non-life), 2016 vs. 2015

Slide 18: Own funds for life and non-life insurers, 2011-2016, SCR coverage ratios, 2015-2016

Slide 19: Number of insurance agents by type and number of sales reps (OFWCA), 2012-2015

Slide 20: Insurance – Regulatory institutions, 2016

Slide 21: Private health Insurance – Opportunity for insurers

3. Non-life insurance Slide 22: Non-life insurance markets in CEE – Size vs. growth matrix, 2014-2016

Slide 23: Non-life premiums per capita & premiums/GDP penetration – CEE comparison, 2016

Slide 24: Non-life insurance gross and net premium evolution, 2012-2016

Slide 25: Top 10 non-life insurance players in Poland, 2016

Slide 26: Market shares of top non-life players evolution, 2013-2016

Slide 27: Non-life premium by client segment and insurance class (car insurance vs. other), 2016

Slide 28: Non-life premium by risk class, 2014-2016

Slide 29: Sales channels of non-life insurance, 2013-2015

Slide 30: Non-life insurers results, technical and P&L accounts, 2016

Slide 31: Non-life insurance - Profitability tree, 2012-2016

Slide 32: Non-life insurance - Claims and expense ratio evolution, 2012-2016

Slide 33: Non-life insurance - Combined ratio and its elements, 2012-2016

Slide 34: Non-life insurance - Acquisition costs evolution, 2014-2016, acquisition costs for top non-life insurers comparison, 2015

Slide 35: Network multi-agents: Unilink, Consultia, CUK, Conditor, LGK etc.

Slide 36: Car insurance - Premium and no. policies evolution, MTPL, Casco, 2012-2016

Slide 37: Car insurance - Top players in MTPL and in Casco, 2014-2016

Slide 38: Car insurance - Combined ratio and its elements, MTPL and in Casco, 2014-2016

Slide 39: Car insurance - Average premium per policy for Casco and TPL, 1Q2012-4Q2015

Slide 40: Car insurance - Usage-based insurance: YU! – Yanosik Ubezpiecza, Link4 & NaviExpert

4. Life insurance Slide 41: Life insurance markets in CEE – Size vs. growth matrix, 2014-2016

Slide 42: Life premiums per capita & premiums/GDP penetration – CEE comparison, 2016

Slide 43: Life insurance gross and net premiums evolution, 2012-2016

Slide 44: Top 10 life insurance players in Poland, 2016

Slide 45: Market shares of top life players evolution, 2014-2016

Slide 46: Life premium by insurance class and segment, 2016

Slide 47: Life premium by risk class evolution, 2014-2016

Slide 48: Life insurance technical reserves evolution and structure, 2012-2016

Slide 49: Sales channels of life insurance, 2013-2015

Slide 50: Life insurers results, Technical and P&L accounts, 2016

Slide 51: Life insurance - profitability tree, 2012-2016

Slide 52: Life insurance - acquisition costs evolution, 2014-2016, acquisition cost ratios for top life insurers, 2015

5. Bancassurance & alternative sales channels Slide 53: Bancassurance: Premium written by bank channel (life/non-life), 2013-2015 – data by KNF vs. data by PIU

Slide 54: Bancassurance: Product/class split in bank channel (life/non-life), 2016

Slide 55: Bancassurance: Sales of investment type life products other than unit-linked, 2012-2016

Slide 56: Bancassurance: Comparison websites and online sales sites of banks - overview

6. Top players' profiles Slide 57: Non-life insurance: PZU, 2014-2016

Slide 58: Non-life insurance: Ergo Hestia, 2014-2016

Slide 59: Non-life insurance: Warta, 2014-2016

Slide 60: Life Insurance: PZU Życie, 2014-2016

Slide 61: Life Insurance: Aviva, 2014-2016

Slide 62: Life Insurance: Open Life, 2014-2016

7. Forecast Slide 63: Non-life insurance premiums forecast, 2017-2019

Slide 64: Life Insurance premiums forecast, 2017-2019

Slide 65: Notes on Methodology

Research Report: Insurance market in Poland, 2017-2019

Research Report: Insurance market in Poland, 2017-2019