The impact of COVID-19 on the insurance sector in Poland has been noticeably across various product classes e.g. falling premium in car insurance or growing premium in property/accident insurance. However, the overall effect on the sector can be assessed as close to neutral. Premium in non-life segment remained flat in Q1-Q3 2020 if compared to the same period of the previous year. By contrast, within life insurance, premium contracted by ~3% YoY, however, the fall was not directly connected to COVID-19 but rather, it was a continuation of a long-term declining trend in life insurance-based investment products suffering from increasingly restrictive regulations.

Tighter regulations are also quoted among triggers of recently observed consolidation.

A few new M&A deals were announced in 2020, including withdrawal of AXA - to be acquired by Uniqa and Aegon to be purchased by VIG. Moreover, an even bigger transaction is in the cards for 2021 as Aviva considered disposing its Polish business

For more information on recent developments in the Polish insurance sector, please refer to the full publication.

Table of contents

Slide 1: Executive summary

1. Macroeconomic overview Slide 2: Poland – Overview and key facts

Slide 3: Poland in Europe: Number of households vs. wealth, 2019

Slide 4: Key macroeconomic indicators, 2015-2020F

Slide 5: Foreign trade statistics, C/A, FDI, 2015-2020F

Slide 6: Unemployment and salaries/wages, 2015-2020F

Slide 7: Disposable income in households and income distribution, 2015-2020F; Income distribution 2019

Slide 8: Consumer confidence index evolution, Dec. 2013 – Oct.2020

Slide 9: Warsaw Stock Exchange - Turnover, Market cap. and indexes, 2014-2019

Slide 10: Banking assets evolution, 2015-Q1 2020

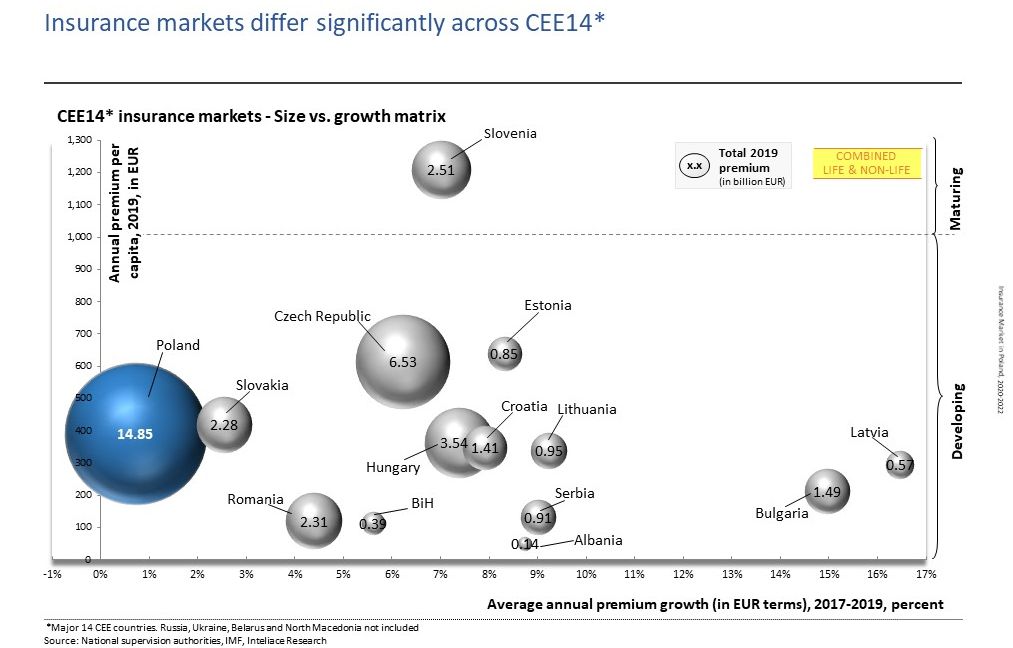

2. Insurance market Slide 11: Insurance Markets in CEE – Size vs. growth matrix, 2017-2019

Slide 12: Insurance premiums per capita & premiums/GDP penetration – CEE comparison, 2019

Slide 13: Insurance gross premiums - Local insurers (life/non-life, in EUR), 2016-2020F

Slide 14: Insurance gross premiums - Local insurers (life/non-life, in PLN), 2016-2020F

Slide 15: Top 10 insurance groups in Poland by total premium written, 1H 2020 (taking into account recently announced M&A)

Slide 16: Insurance market concentration and Herfindahl-Hirschman Index (life/non-life), 1H 2019 vs. 1H 2020

Slide 17: Current and upcoming Insurance M&A transactions in Poland, 2018-2020

Slide 18: Own funds for life and non-life insurers, 2016-1H 2020, SCR coverage ratios, 2017-2019

Slide 19: Number of insurance agents by type and number of sales reps (OFWCA), 2017-2019

Slide 20: Insurance – Regulatory institutions

Slide 21: Private health Insurance – Opportunity for insurers; Premium written, 2017-2020F

3. Non-life insurance Slide 22: Non-life insurance markets in CEE – Size vs. growth matrix, 2017-2019

Slide 23: Non-life premiums per capita & premiums/GDP penetration – CEE comparison, 2019

Slide 24: Non-life insurance gross and net premium evolution, 2016-2020F

Slide 25: Top 10 non-life insurance players in Poland, 1H 2020

Slide 26: Market shares of top non-life players evolution, 2017-1H 2020

Slide 27: Non-life premium by client segment and insurance class (car insurance vs. other), 1H 2020

Slide 28: Non-life premium by risk class, 2018-1H 2020

Slide 29: Sales channels of non-life insurance, 2018-2019

Slide 30: Non-life insurers results, technical and P&L accounts (waterfall chart), 2019

Slide 31: Non-life insurance - Profitability tree, 2016-1H 2020

Slide 32: Non-life insurance - Claims and expense ratio evolution, 2016-1H 2020

Slide 33: Non-life insurance - Combined ratio and its elements, 2016-1H 2020

Slide 34: Non-life insurance - Acquisition costs evolution, 2018-1H2020, acquisition cost ratios for top non-life insurers, 2019

Slide 35: Network multi-agents: Unilink, CUK, Conditor, LGK , Asist, Arrant, DCU etc.

Slide 36: Current legislative initiatives affecting insurance business in Poland, 2017/2019

Slide 37: Car insurance - Premium and no. policies evolution, MTPL, Casco, 2016-1H 2020

Slide 38: Car insurance - Top players in MTPL and in Casco, 2018-1H 2020

Slide 39: Car insurance - Combined ratio and its elements, MTPL and in Casco, 2018-1H 2020

Slide 40: Car insurance - Average premium per policy for Casco and TPL, 1Q2015-3Q2020

4. Life insurance Slide 41: Life insurance markets in CEE – Size vs. growth matrix, 2017-2019

Slide 42: Life premiums per capita & premiums/GDP penetration – CEE comparison, 2019

Slide 43: Life insurance gross and net premiums evolution, 2016-2020E

Slide 44: Top 10 life insurance players in Poland, 1H 2020

Slide 45: Market shares of top life players evolution, 2017-1H 2020

Slide 46: Life premium by insurance class and segment, 1H 2020

Slide 47: Life premium by risk class evolution, 2018-1H 2020

Slide 48: Life insurance technical reserves evolution and structure, 2017-1H 2020

Slide 49: Sales channels of life insurance, 2018-2019

Slide 50: Life insurers results, Technical and P&L accounts (waterfall chart), 2019

Slide 51: Life insurance - profitability tree, 2016-1H 2020

Slide 52: Life insurance - acquisition costs evolution, 2018-1H 2020, acquisition cost ratios for top life insurers, 2019

5. Bancassurance Slide 53: Bancassurance: Premium written by bank channel (life/non-life), 2017-2019,data by KNF vs. data by PIU

Slide 54: Bancassurance: Product/class split in bank channel (life/non-life), 3Q 2020

Slide 55: Bancassurance: Sales of investment type life products other than unit-linked, 2016-2020F

Slide 56: Bancassurance: Comparison websites and online sales sites of banks – overview, 2020

6. Top players' profiles Slide 57: PZU - Powszechny Zakład Ubezpieczeń

Slide 58: Warta (Talanx)

Slide 59: ERGO Hestia

7. Forecast Slide 60: Non-life insurance premiums forecast, 2020-2022

Slide 61: Life Insurance premiums forecast, 2020-2022

Slide 62: Notes on Methodology

Research Report: Insurance market in Poland, 2020-2022

Research Report: Insurance market in Poland, 2020-2022